Slow and Steady Decline but Who Wins the Race?

Peter Bernstein, Chief Economist, pbernstein@rcfecon.com, 312-431-1540 x1515

The Current Situation

The CPI increased 0.1% in November reducing the year-over-year inflation rate to 3.1%. Core prices rose 0.3% leaving the core inflation rate at 4.0%. Inflation has been on a downward trend through 2023 and if the current trend continues, the economy will reach the Fed’s 2% inflation goal sometime next summer.

There is a downhill race going on between inflation and employment. Both are slowing so the big question is which slows more quickly. Will the economy reach 2% inflation with employment growth still positive as suggested by the chart below? Or will employment growth decline more rapidly resulting in job losses before the Fed’s 2% goal is reached? One thing seems certain: the Fed is committed to getting inflation down to 2% and isn’t going to abandon this task even if employment begins to fall.

This is where the stickiness of core inflation becomes a problem. While the headline inflation rate has fallen by two-thirds since its peak at 9.1% in mid-2022, core inflation’s decline has been more subdued. And core inflation has always been the Fed’s focus. At 4%, it remains double the target rate, showing that while inflation trends are moving in the right direction, there is still quite a way to go.

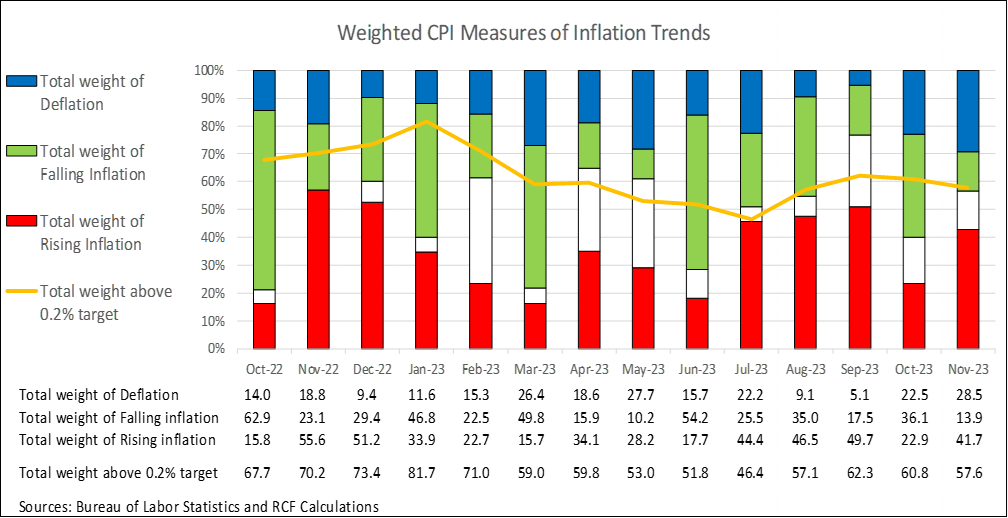

RCF’s Inflation Scorecard

RCF’s Inflation Scorecard is based on analysis of 20 different price series comprising 98% of the total consumer price index. Each of these price series represents a portion of the CPI based on household spending patterns. For example, food purchased for at-home consumption is about 8.7% of the typical consumer’s budget; it has a weight of 8.73 out of a total index of 100.

Our scorecard presents two metrics to track month-to-month price increases. The first metric is the share of the index for which inflation in the most recent month is rising (greater than the prior month’s inflation) vs. the share of the index for which inflation is falling (lower than the prior month) or prices fell (deflation). Because deflation is showing up across more categories, we’ve added a separate measure of the total weight of deflation within the CPI index.

Our second metric is the share of the index for which the most recent month’s inflation exceeded 0.2%, a monthly rate that corresponds to the Federal Reserve’s target inflation rate of 2% per year.

RCF Inflation Scorecard: November 2023

The scorecard metrics for November were a decidedly mixed bag. The good news is that 28% of the weighted CPI had a lower price in November than in October, the highest share of deflation within the CPI since inflation began rising more than two years ago. Given prices are notably higher than they were two years ago, a growing share of the CPI experiencing price declines will do a lot to offset those price increases.

The bad news is that 42% of the CPI had higher inflation in November than in October, a sharp reversal from October when only 23% of the CPI experienced rising inflation. Overall, 58% of the CPI had November inflation above 0.2%, a similar share to what we have seen over the past several months.

Analysis of Individual Components of the Consumer Price Index

Sources: Bureau of Labor Statistics and RCF Calculations. 1. Inflation direction indicates whether monthly inflation in November was higher or lower than monthly inflation in October. Deflation means prices fell in November vs. October.

Highlights:

- Deflation was a big story in November with eight of our 20 CPI categories experiencing a price decline in the month. In addition to the continued decline in motor fuel prices (down 6% in November following a 4.9% decline in October), other categories with falling prices included alcoholic beverages, household furnishings, and apparel which should brighten people’s holiday shopping this year.

- New vehicle prices also fell a bit in November, the second straight month with a small price decline. Used car and truck prices bucked their recent downward trend by rising 1.6% in November, though they are still down 3.8% compared to a year ago.

- Food-at-home prices rose just 0.1% in November and are only 1.7% higher than a year ago. However, food away from home continues to show higher inflation, 0.4% in November and 5.3% year-over-year.

- Rent prices rose 0.5% in October, same as September, and owner’s equivalent rent (OER) inflation ticked up from the prior month. The path to 2% inflation will require a sharp drop in shelter price inflation which, unfortunately, remains close to 7%.

- Five categories (household energy, used cars and trucks, motor fuel, public transportation, and education/communication) have lower prices now than they did a year ago. But all together, these five only account for just 16% of the weight of the CPI, half that of rent and OER. This again shows that the path to 2% inflation runs through the housing market.