February 4, 2021

Our guide to notable economic data, forecasts, and analyses. For more information contact Peter Bernstein at pbernstein@rcfecon.com. Additional updates and releases can be found at www.rcfecon.com/research/news-and-press-releases/

- Bureau of Economic Analysis, Personal Income and Outlays, December 2020

- U.S. Census Bureau, Construction Spending, December 2020

- U.S. Census Bureau, New Home Sales, December 2020

- IHS Markit, Monthly GDP Index, December 2020

- University of Michigan, Surveys of Consumers, January 2021 (final)

- Congressional Budget Office, Economic Outlook: 2021 to 2031, February 2021

- Brookings, The Macroeconomic Implications of Biden’s $1.9 Trillion Fiscal Package

- Chart of the Week – Comparison of CBO’s Recent Economic Forecasts

Data Releases

Bureau of Economic Analysis, Personal Income and Outlays, December 2020

In December 2020, personal income increased +0.6% compared to November while consumer spending fell -0.2%. According to Marketwatch, both of these were better than consensus of +0.1% and -0.4% respectively. https://www.bea.gov/news/2021/personal-income-and-outlays-december-2020, https://www.marketwatch.com/economy-politics/calendar

U.S. Census Bureau, Construction Spending, December 2020

In December 2020, total construction spending was +5.7% compared to December 2019. The value of construction in 2020 was +4.7% compared to 2019. Residential construction was up +20.7% in December 2020 compared to December 2019 while non-residential was -4.8%. https://www.census.gov/construction/c30/pdf/release.pdf

U.S. Census Bureau, New Home Sales, December 2020

In December 2020, sales of new single-family houses were 842,000, +15.2% compared to December 2019. https://www.census.gov/construction/nrs/pdf/newressales.pdf\

IHS Markit, Monthly GDP Index, December 2020

“Monthly GDP was essentially flat in December following a 1.2% decline in November that was revised lower by 0.4 percentage point. The flat reading in December reflected declines in personal consumption expenditures and inventory investment that were essentially offset by increases in nonresidential fixed investment, residential fixed investment, net exports, and the portion of monthly GDP not covered by the monthly source data. The level of GDP in December was 1.7% below the fourth-quarter average at an annual rate.” https://cdn.ihsmarkit.com/www/pdf/1020/US-Monthly-GDP-Current-Index.pdf

University of Michigan, Surveys of Consumers, January 2021 (final)

The Index of Consumer Sentiment was 79.0 in January 2021 compared to 80.7 in December 2020. The index for Current Economic Conditions fell more noticeably from 90.0 in December to 86.7 in January. Meanwhile the Index of Consumer Expectations was 74.0 in January compared to 74.6 in December. http://www.sca.isr.umich.edu/

Economic Forecasts and Analyses

Congressional Budget Office (CBO), Economic Outlook: 2021 to 2031, February 2021

Key takeaways: Real GDP growth is forecasted to grow 3.7% in 2021 (fourth quarter to fourth quarter) and average 2.6% over the next five years. Real GDP is expected to attain its prepandemic level sometime in 2021. However, the gap between real GDP and potential GDP is expected to persist until 2025. In 2021, average monthly payroll employment is forecasted at 521,000. The unemployment rate is forecasted to fall to 5.3% in 2021, and further to 4% between 2024 and 2025. Labor force forecast to recover to its prepandemic level in 2022. However the employment level does not return to its prepandemic level until 2024.

The CBO’s February 2021 forecast “incorporates economic and other information available as of January 12, 2021, as well as estimates of the economic effects of all legislation (including pandemic-related legislation) enacted up to that date.” As such, it does not assume any new stimulus, including the President Biden’s proposed $1.9 trillion dollar plan. https://www.cbo.gov/system/files/2021-02/56965-Economic-Outlook.pdf

Brookings, The Macroeconomic Implications of Biden’s $1.9 Trillion Fiscal Package

“The Biden Administration recently proposed an additional $1.9 trillion in federal spending to address the ongoing pandemic. We estimate that the package would boost economic activity, as measured by the level of real gross domestic product (GDP), by about 4 percent at the end of 2021 and 2 percent at the end of 2022, relative to a projection that assumes no additional fiscal support. We project that if the Biden package were enacted, GDP would reach the Congressional Budget Office’s (CBO) pre-pandemic GDP projection after the third quarter of 2021, exceeding it by 1 percent in the fourth quarter. In the middle of 2022, GDP would show a temporary and shallow decline and then grow at an annual rate of about 1.5 percent, coming close to the path projected just before the pandemic.”

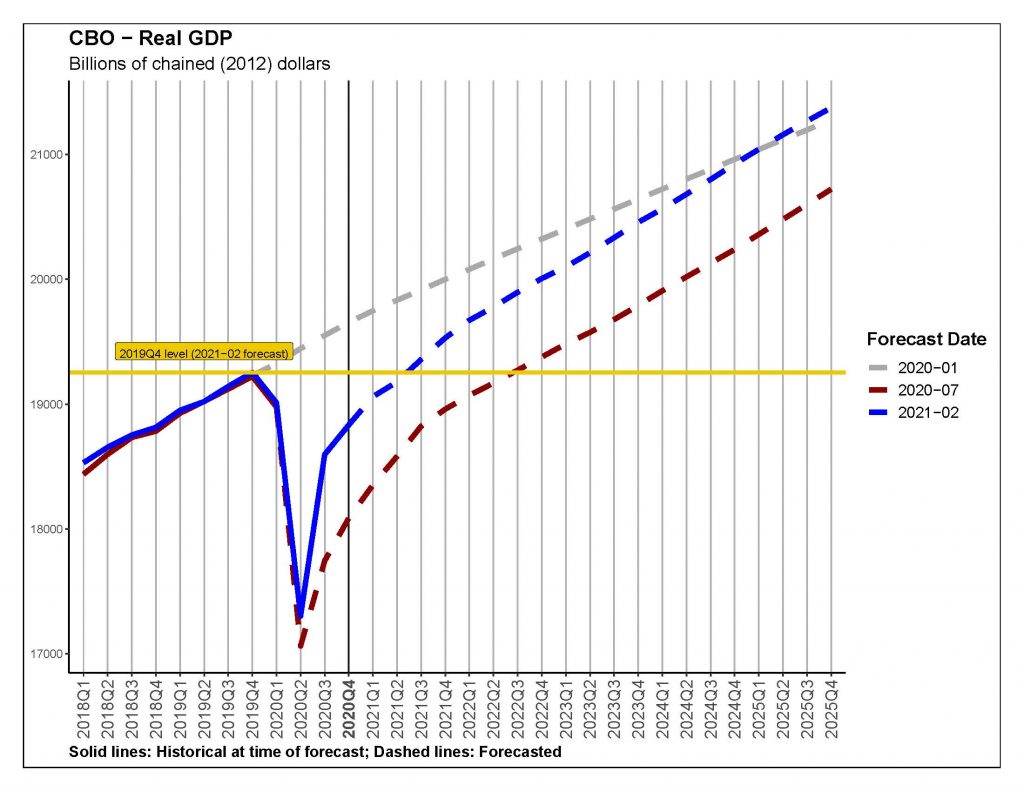

Chart of the Week – Comparison of CBO’s Recent Economic Forecasts

The CBO’s economic forecast released this week, is notably more optimistic than their forecast from July 2020. The reasons for this are because “the downturn was not as severe as expected and…the first stage of the recovery took place sooner and was stronger than expected”.

The CBO’s prepandemic (January 2020) as well as their July 2020 and February 2020 forecasts of real GDP are show below. Real GDP is expected to reattain its prepandemic peak (the 2019Q4 level) sometime in mid-2021. The July 2020 forecast had this occurring in mid- to late-2022.